While reading a business article the other day, I came across a passage where the writer reminded the reader of the importance of hearing the signal through the noise. Through all the political noise, I have been studying and analyzing the changes occurring on Wall Street in relationship to the housing markets.

Today, the signal we will discuss is the major shift in Wall Street investments from oil and minerals industries to our housing markets, including multifamily. I thoroughly explain this phenomenon in my book, Stealing Home: How Artificial Intelligence Is Hijacking the American Dream. However, today we will limit our discussion to proforma appraisals and the ever-increasing rents that support them. Let me explain.

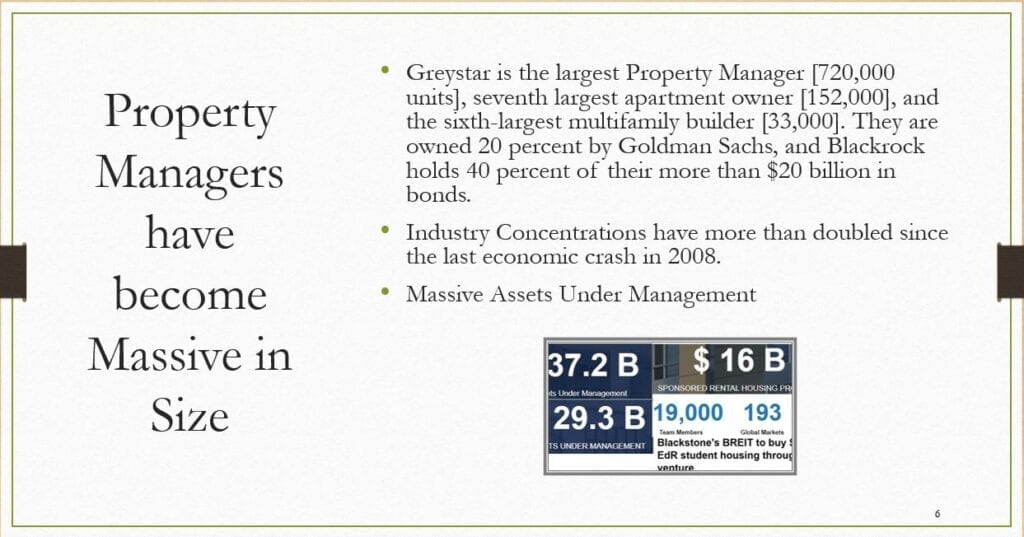

The entire rental housing industry, driven by Artificial Intelligence Technology, has undergone a complete transformation in the past few years. The Property Managers have become massive in size and now operate through vertical trust organizations. Wall Street and the housing industry are making massive bets—at the taxpayer’s expense.

You see, the tax-credit syndicators who are capable of generating the institutional investor-owned properties are forming a complex, fragmented ownership-style structure. These structures have become so complicated, and the structures the owners create to hold their assets have equally become so complex, that in response, in November 2018, Julie Segal reported in the Institutional Investor that J. P. Morgan had issued a new study for the firm’s wealthiest clients, warning that those assets may be hard to sell once the economy goes south.

Today, Fannie Mae, Freddie Mac, and the Federal Housing Administration underwrite almost $7 trillion in mortgage-related debt, 33 percent more than before the 2008 housing crisis. But, what is behind those loans and offsetting bonds? How solid are they? The 2008 Great Recession saw nearly 30 percent of the multifamily CMBS loans end in default, and the entire multifamily housing sector suffered catastrophic losses. Nevertheless, today, rental incomes continue to show an ever-increasing profit margin based on rental rate increases. Perhaps more important, are those ever-rising rental rates sustainable? The question is asked because those ever-increasing rents give value to the 7 trillion dollar debt.

According to a recent Reis report, we now have more multifamily units under construction than at any time since the mid-1970s, which long-held the record. In fact, the year 2017 was the most active on record for multifamily real estate finance.

Lack of Regulation and Oversight

The summary of the four (4) economic studies I performed concluded that this industry has altogether acquired the ability to avoid regulatory oversight. No one is watching. For example, in 2018, the Office of Inspector General (OIG) reported that the Government Sponsored Enterprises (GSEs) failed to perform required internal credit and operational audits on Fannie Mae and Freddie Mac (the primary entities responsible for the rental housing industry). Furthermore, the GSEs haven’t completed the examinations for several years. In 2018, the OIG stated that “GSE management accountable for the quality and types of loans they are putting on their books had been purposefully kept out of the decision-making process.”

Additionally, the GSEs are not adhering to approved underwriting guidelines. For example, many of the loans are underwritten with Loan To Value Ratios exceeding 80 percent and usually much higher with mezzanine financing. Worse yet, for all practical purposes, the loans are non-recourse [not guaranteed by the owners], leaving the taxpayers to bear all the risk. The Rental Market Industry property owners are taking on massive high-risk debt in the financing of these properties.

History of Proforma-Based Appraisal Theory

In 1982, when beginning my work as a Federal Bank Regulator, the Farm Credit System had already been experiencing economic upheaval due to their lending in the Aquatic Industry—fishing vessels. In their mad rush to grow loan volume and increase the bottom line (ROI), the Farm Credit System began financing an industry they knew little about. Part of their process to grow loan volume included the weakening of credit and underwriting policies, including the appraisals’ policy.

In fact, by the time I arrived, the inside joke amongst the Federal Regulators was that appraisals completed by MAI—Member of the Appraisal Institute (provided what was known as MAI Appraisals)—once the benchmark of trust, now had the derogatory meaning: “Made as Instructed (MAI).” The Farm Credit Banks would take on massive credit losses due to both their weak underwriting standards and, in part, to the Federal Regulators’ lax oversight.

At the center of the crisis were the standards of the appraisal (theories) themselves, which, over time, had weakened. This resulted from constant pressure from the member banks to lessen credit standards, as they deemed those standards to be the very roadblock to loan growth—the inability to compete against the big banks like Wells Fargo and Bank of America.

When Congress authorized the Aquatic Lending program, the lending rules were already established as part of the approval process. Initially, the appraisals were required to provide a value based on the theory of “As-Is” Market Value; in other words, the property’s value at a point in time—in this case, at the time of loan consideration.

However, because the original credit standards were weakened, appraisals were allowed to provide values based on certain assumptions, such as ever-increasing market growth and/or ever-increasing market prices. This assumption is steeped in Proforma-based theory. This theory concludes, among other aspects, the ability to forecast and give present value to future events such as price increases and allow those projected future possibilities to influence the current As-Is Value. The result of the changes in theory (credit policy) was that Farm Credit achieved and surpassed their loan goals. The value of the fishing vessels skyrocketed, and Proforma-Based Appraisals supported those ever-increasing values. You see, over the many years, I have learned that there is a correlation between ease of access to seemingly endless amounts of credit and skyrocketing values of that financed property, in this instance, fishing vessels—today apartment buildings.

Unfortunately for the Farm Credit System, the entire agriculture industry would enter into one of its worst economic downturns, which lasted for decades. Most unfortunate was the fact that Farm Credit had severely depleted their loan-loss reserves to cover loan losses from the aquatics division, which left them entirely unprepared financially for the oncoming crisis. The taxpayers would provide bailouts to save the lending system.

Today, appraisers are utilizing Proforma-Based Values supported by projected rents rather than values based on historical data. The practice of using Proforma-based income statements to support Appraised Values, which are dependent on sizable rental rate increases going forward, has become the norm as a new breed of investors enters the market. However, no one seems to be paying attention to the ability or sustainability of those rental rate increase projections. Can the tenants afford those rental rate increases?

In chapter four of my book, I go into detail explaining the results of a study I completed on the sustainability of those projected ever-increasing rents.

What are your thoughts?